Self-Storage in 2026: From Pandemic Surge to Mature, Predictable Returns

The self-storage sector has long been a quiet workhorse of real estate: simple, resilient, and surprisingly versatile. But few periods have drawn as much attention as the pandemic years of 2021-2022, when occupancy soared to unprecedented levels, driven by sudden shifts in how people lived, moved, and stored their belongings.

That surge, while remarkable, was never a new baseline. Industry occupancy peaked near 96.5% in 2021 before normalizing to approximately 90% by 2024-2025[1], a level consistent with long-term historical averages. The pandemic compressed years of demand into a short window, temporarily obscuring the sector’s true operating profile rather than redefining it.

As those conditions have unwound, performance has normalized. Occupancy has stabilized near 90%, a level that reflects normalization following pandemic-era dislocations rather than structural weakness. For investors, the key question is no longer whether self-storage can grow rapidly, but how it performs when growth gives way to discipline.

What follows is a framework for understanding self-storage in its next phase, where maturity is reshaping demand durability, market structure, and long-term returns.

This article reflects insights shared by Spartan Investment Group Co-Founder and CIO Ryan Gibson, who recently appeared on an Institutional Real Estate, Inc. podcast episode discussing the sector’s transition from pandemic-driven growth to a more disciplined, execution-focused phase. For readers interested in a deeper operator-level view, the full episode offers additional context on market dynamics and investment discipline.

The Five D’s Behind Self-Storage Demand

Self-storage demand is rarely aspirational. It shows up when something changes (often quickly) and space becomes a constraint. Unlike discretionary real estate uses, storage is activated at moments of transition, when households and businesses need an immediate, flexible solution. That dynamic has held across cycles and is central to the sector’s durability.

The remaining demand comes largely from small businesses that use storage as functional infrastructure. These tenants are not seeking visibility or build-out; they are solving for proximity, flexibility, and cost. Their use of storage as an operational extension (often involving larger units and longer stays) adds another layer of stability to overall utilization.

Taken together, these demand sources produce a profile defined by persistence rather than cyclicality. In practice, that means more predictable occupancy, less volatility through economic slowdowns, and a utilization pattern that resembles a service necessity more than a discretionary expense.

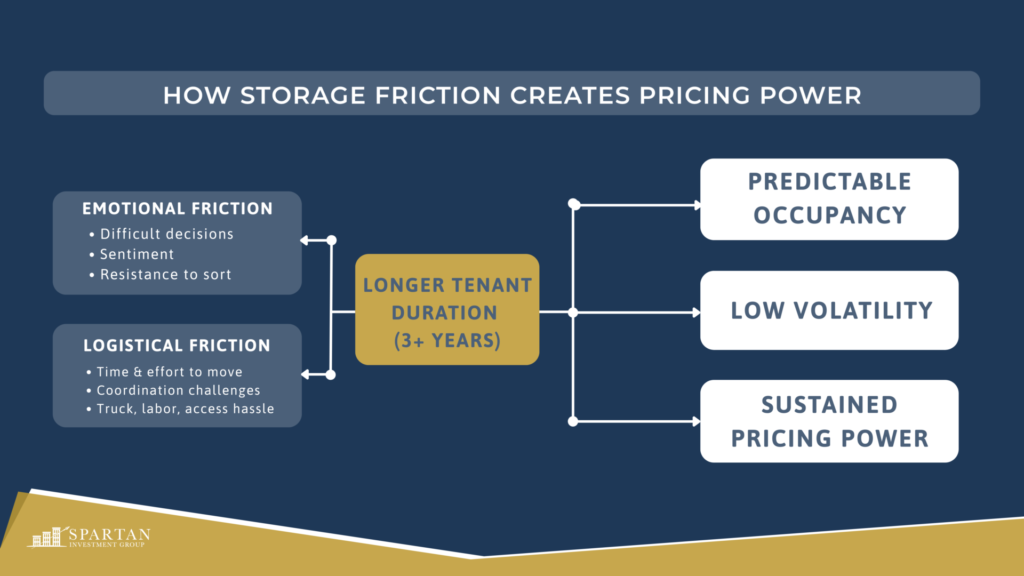

Why Storage Customers Stay: Emotional + Logistical Friction

Self-storage is a surprisingly “sticky” business. The average customer stays around three years, and many who enter expecting short-term use end up remaining far longer.

That persistence is driven by emotional and logistical friction. Moving belongings in and out takes time, effort, and coordination, while deciding what to part with carries emotional weight. Together, those frictions discourage churn and turn “temporary” storage into a default long-term solution.

For operators and investors, even as market growth normalizes, the result is:

- predictable occupancy

- low volatility

- historically supported pricing power

In essence, storage is not just a place to put things. It is a durable, recurring revenue stream anchored in how people behave when change meets attachment.

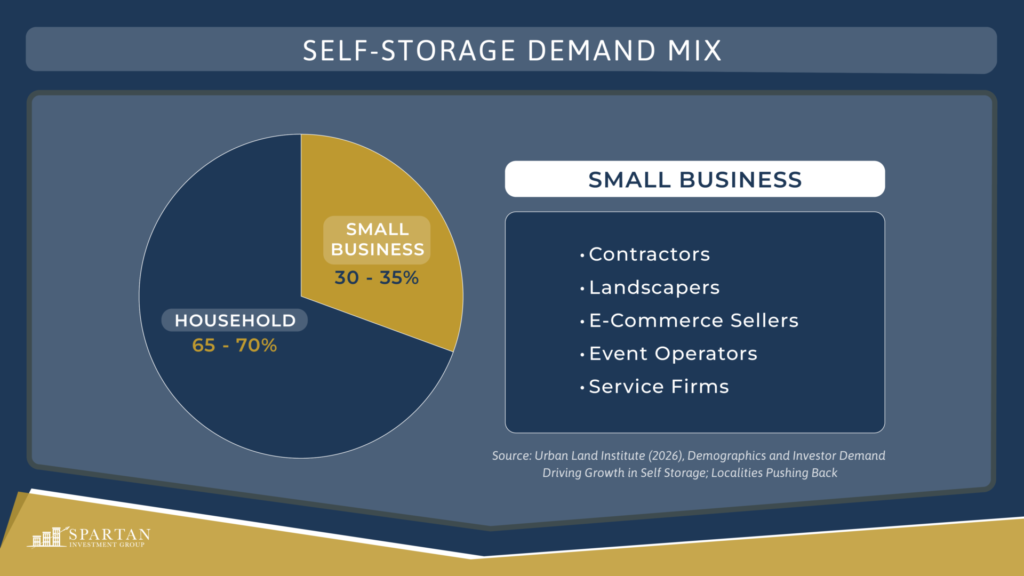

Commercial Demand as a Stabilizing Force

Roughly one-third of all self-storage demand comes from small businesses[2], and this share has been steadily rising as space becomes more expensive and more regulated.

Contractors, landscapers, e-commerce sellers, event operators, and service businesses increasingly rely on storage as flexible operating space, a place for inventory, tools, records, and regional staging without long leases, build-outs, or zoning complexity. HOA restrictions and shrinking residential space have only accelerated this shift.

Unlike household storage, business demand is structural rather than transitional, with many operators reporting multi-year tenancies and multiple-unit usage among commercial customers.

For investors, this demand provides a powerful stabilizer: long-term, non-cyclical occupancy that strengthens cash flow predictability in a maturing market.

Performance Divergence: Operator Quality Matters

The recent softening in self-storage performance is often misunderstood. It reflects reduced household mobility, driven in part by mortgage-rate lock-in, rather than a breakdown in underlying demand. Fewer people moving means fewer short-term storage needs, but the core drivers of the business remain intact.

What has changed is that results now diverge sharply by market and by operator. In a mature asset class, broad tailwinds no longer lift every facility equally. Performance is determined by micro-location, pricing discipline, marketing, and asset design.

The clearest underperformers today are not “bad storage markets,” but overbuilt or oversized facilities delivered into trade areas that could not absorb them. These projects distort local pricing and occupancy, but they are local supply errors, not evidence of structural weakness across the sector. In many cases, underperformance stems from facilities scaled beyond what local demand could support, a problem that is fundamentally site-level, not sector-wide.

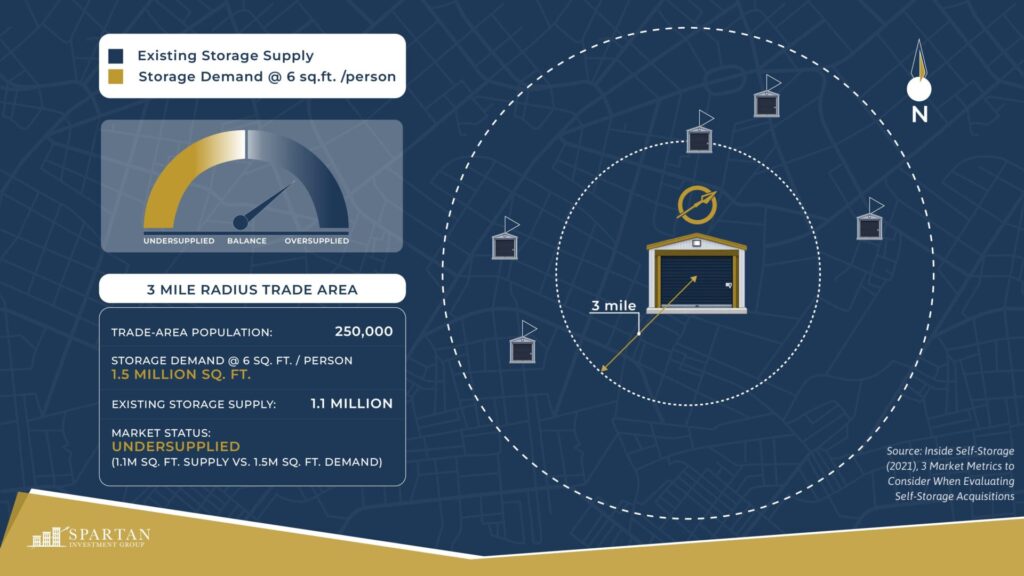

Self-storage must be evaluated on a hyper-local basis: most customers live or work within a three mile radius of their facility[3], and a market that appears overbuilt at the metro level may be undersupplied within a specific three-mile ring.

In this phase of the cycle, self-storage behaves like institutional real estate should: execution matters. The winners are those who understand their three-to-five-mile trade areas, manage revenue actively, and operate assets scaled to real demand, not boom-era assumptions.

Market Fundamentals & Saturation

At the national level, self-storage demand averages roughly six square feet per person[4], though functional demand varies meaningfully by housing stock and climate. Local conditions matter. Markets without basements[5] or attics (such as much of Texas) can support materially higher saturation, while regions with more in-home storage capacity, including parts of the Pacific Northwest, require less.

As the sector matures, location quality increasingly determines performance. Dense residential infill areas, markets with zoning constraints, and municipalities resistant to new development tend to exhibit greater long-term stability by limiting future supply. In these environments, existing assets benefit from natural barriers to entry rather than relying on demand acceleration.

Operator discipline further separates outcomes. In balanced or fully built markets, pricing resilience is driven by revenue management, unit mix optimization, and cost control, not by incremental supply growth. Saturation alone does not dictate returns; how well an asset is positioned and managed within its trade area does.

In a normalized cycle, self-storage rewards precision over expansion, a dynamic that favors experienced operators in supply-constrained markets.

Regulatory Environment: Storage as Infrastructure

As self-storage has matured, it has become increasingly visible to municipalities and more regulated as a result. Cities often resist new facilities because they generate limited employment and occupy valuable land. In many markets, storage now requires conditional-use permits, special hearings, or faces outright zoning exclusions.

For operators and investors, however, this resistance is often a feature, not a flaw.

Zoning friction acts as a supply constraint, protecting existing assets from future competition. Markets where local governments have tightened approvals tend to see more stable occupancy and stronger long-term pricing, because new capacity cannot easily flood the trade area.

At the same time, regulators are implicitly recognizing storage as utility-like infrastructure. In several states, the imposition of sales tax on self-storage further reflects its evolution from a discretionary product into utility-like infrastructure. Households and businesses rely on storage the way they rely on parking, broadband, or logistics hubs. It supports how people live and work, even if it does not look like traditional commercial real estate.

In a mature cycle, regulatory barriers increasingly shape outcomes. The most durable assets will be those embedded in high-demand, supply-restricted markets, where zoning, land scarcity, and political friction preserve long-term value.

Why Self-Storage Remains a Professional Asset

Self-storage has evolved into a mature, execution-driven real estate sector, where outcomes are shaped less by macro tailwinds and more by operator discipline and micro-market selection.

The asset class offers a rare combination of predictable cash flow, pricing flexibility, and low capital intensity. Short-term leases allow operators to reset rents quickly, while minimal tenant improvements and limited physical depreciation preserve margins and reduce reinvestment risk. In stable or flat-growth environments, these traits translate into consistent, defensible income.

Just as important, self-storage is now supported by institutional-grade data, revenue management, and operating platforms. What was once a fragmented, mom-and-pop industry has become a professionalized ecosystem capable of underwriting, pricing, and managing assets at scale.

The result is an asset class defined not by volatility, but by structural durability. In 2026 and beyond, self-storage remains compelling not because it is booming, but because it functions as a reliable, utility-like component of modern real estate portfolios, one where disciplined execution is rewarded with long-term, repeatable returns.

For investors looking to apply this framework in practice, Spartan Investment Group is actively deploying capital in markets that reflect these principles, favoring infill locations, disciplined supply profiles, and durable demand drivers. Our current Rockies portfolio offering is one example of how we are positioning assets for long-term, execution-driven returns.

Disclaimer: This article is for informational and educational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any securities or investment products. The views expressed are based on current market observations and publicly available data and are subject to change. Past performance and market trends are not indicative of future results. Any forward-looking statements involve risks and uncertainties, and actual outcomes may differ materially. Investors should conduct their own due diligence and consult with their financial, legal, and tax advisors before making investment decisions.

Sources:

[1] Capright. Self-Storage REIT Update – April 2025. https://www.capright.com/self-storage-reit-update-april-2025/

[2] Urban Land Institute. Demographics and Investor Demand Driving Growth in Self Storage; Localities Pushing Back. https://urbanland.uli.org/development-and-construction/demographics-and-investor-demand-driving-growth-in-self-storage-localities-pushing-back

[3] Newmark. 2024 U.S. Multifamily Market Conditions Report. https://eussa01corpweb.blob.core.windows.net/nmrkweb/uploads/documents/ALM24_Market-Conditions.pdf

[4] Inside Self-Storage. 3 Market Metrics to Consider When Evaluating Self-Storage Acquisitions. https://www.insideselfstorage.com/acquisitions-buying/3-market-metrics-to-consider-when-evaluating-self-storage-acquisitions

[5] Affleck, John. “Unlocking Self-Storage: A Strategic Framework for Market Selection,” CBRE Investment Management, April 22, 2025. https://www.cbreim.com/insights/articles/unlocking-self-storage