How to Evaluate a Syndication Sponsor: 5 Things That Matter Most

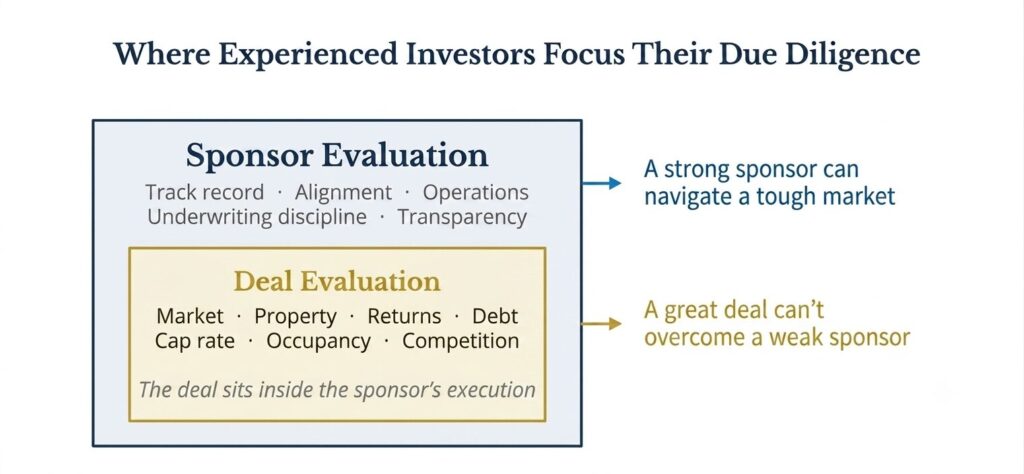

In a real estate syndication, you are investing in the sponsor as much as you are investing in the property. The sponsor selects the market, negotiates the acquisition, structures the capital stack, executes the business plan, manages the asset, and determines the exit. A strong operator may be better positioned to navigate challenges and improve outcomes, while weak execution can impair even an otherwise attractive property. This guide provides a disciplined framework for evaluating the five dimensions of sponsor quality that most directly influence the outcome of your investment.

Why Sponsor Quality Is the Variable Most Investors Underweight

Most first-time passive investors spend the majority of their due diligence evaluating the deal: the property, the market, the projected returns. That is understandable. The deal is tangible: there are photos, a location, a rent roll, and a pro forma full of numbers to analyze.

But many experienced syndication investors place significant weight on sponsor diligence, though both sponsor and deal-level diligence are important. If you could only do due diligence on either the sponsor or the deal, many seasoned investors would choose the sponsor.[1]

The reason is structural. As a limited partner, you have no operational control. You cannot intervene if rents underperform, if construction runs over budget, or if the local market shifts. Your outcome is heavily dependent on the sponsor’s ability to navigate those challenges, and their willingness to prioritize your capital alongside their own.

According to a 2024 survey by CrowdStreet, only 38% of syndication sponsors publicly share full-cycle performance data.[2] This suggests investors should ask whether a sponsor provides full-cycle performance data rather than relying only on projected returns. This information asymmetry makes sponsor evaluation not just important, but essential.

The five dimensions that follow represent the areas where the difference between a strong sponsor and a weak one shows up most clearly in investment outcomes.

Track Record: Realized Performance, Not Projected Returns

One of the most useful indicators of sponsor quality is realized performance, not what they project they will do.

Projected pro formas can be highly sensitive to assumptions, which is why investors should compare projections against realized performance where available. Spreadsheet models are infinitely flexible; as one industry expert noted: “Developers can make those numbers say anything they want. Need a 25% IRR? You got it.”[3] A documented history of realized returns, particularly when complete and consistently presented, can be more difficult to misrepresent than projections.

Full-cycle track record

Has the sponsor taken deals from acquisition through disposition? A sponsor who has acquired, operated, improved, and exited properties has demonstrated the complete skill set required. For strategies that rely on sale proceeds, investors should evaluate whether the sponsor has successfully executed exits, as the exit phase is typically where a significant portion of the projected return is generated.

Realized versus projected performance

Ask to see actual returns from exited deals, not marketing materials from active investments. Compare realized IRR, cash-on-cash, and equity multiple against what was originally projected. Comparing realized results to original projections can help investors evaluate underwriting discipline. Large or repeated variances from projections should prompt further questions about assumptions, execution, and market conditions.

Performance through adversity

How did the sponsor perform during the 2020 COVID disruption? During the 2022–2023 interest rate shock? A track record built entirely during a rising market tells you very little about how the sponsor will manage a downturn. Where applicable, historical performance during stress periods may provide useful context, but does not guarantee future downside protection.

Asset-class specificity

A sponsor with 15 years of self-storage experience is fundamentally different from one with 15 years of multifamily experience who is “pivoting” to self-storage. Operating expertise is asset-class specific. Revenue management, dynamic pricing, digital marketing, and construction management for self-storage differ materially from other property types.

Key Question to Ask

“Can you provide a schedule of all exited investments with original projected returns alongside actual realized returns? How did your portfolio perform during the 2022–2023 rate environment?”

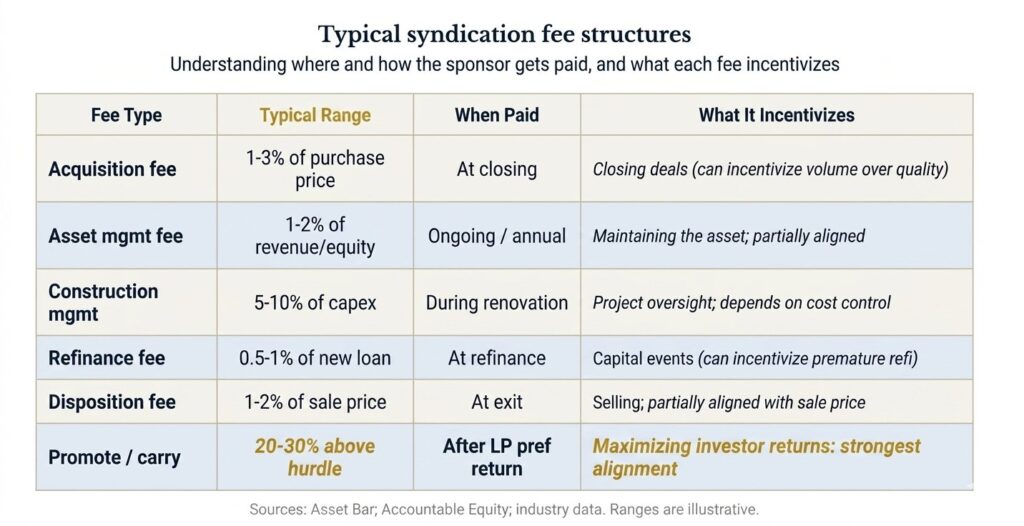

Structural Alignment: How the Deal Is Built Reveals a Lot

Incentive alignment is the structural foundation of a trustworthy syndication. The question is not whether the sponsor is paid (they should be). The question is whether the way they are paid creates incentives that are consistent with investor outcomes.[4]

Heavy upfront compensation can create a potential incentive imbalance if the sponsor’s remaining economics are not meaningfully tied to long-term performance. The former has limited financial motivation to manage the asset well after closing; the latter’s economics are directly tied to the same outcome investors are relying on.

The table above is for educational purposes only. Actual fees vary by offering and should be reviewed in the applicable PPM and operating agreement. The promote / carry row reflects one possible structure; actual alignment depends on the full waterfall as described in offering documents.

Preferred return structure

Does the waterfall include a preferred return to LPs before the sponsor participates in profits? A typical preferred return of 6–8% may provide limited partners with the first distributions until they achieve a specified annual yield on their invested capital.

Waterfall sequencing

Sponsors whose promote is earned only after LPs receive a defined return hurdle may have stronger structural alignment, depending on the full waterfall. Sponsors who earn a fixed percentage of all cash flows from day one offer weaker structural alignment by comparison.

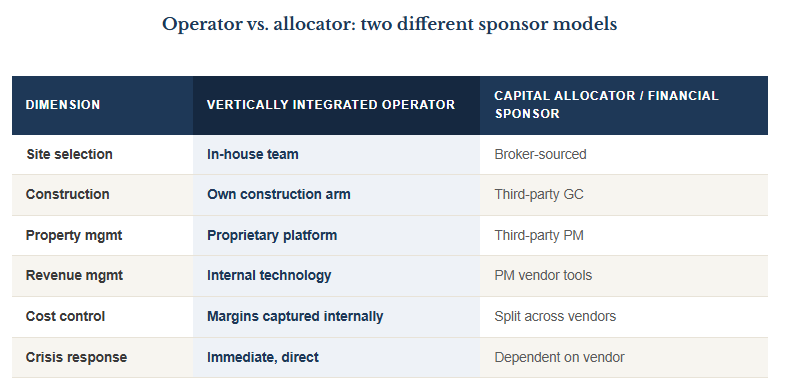

Operational Depth: Operators vs. Allocators

Not all sponsors are created equal in their relationship to the asset. There is a meaningful distinction between a sponsor who operates the property and a sponsor who allocates capital and outsources operations to third parties. Both models can work, but the risk profile is different.

These are general model differences; actual results depend on execution, controls, personnel, market conditions, and third-party partner quality.

In self-storage specifically, operational depth matters because performance is driven by daily decisions: dynamic pricing, digital marketing bid management, call center conversion rates, and expense control at the facility level. A vertically integrated sponsor may have greater direct control over operational levers that can affect asset performance.

At Spartan Investment Group, vertical integration is a core part of our strategy. Through FreeUp Storage, we manage or oversee key dimensions of the asset lifecycle across many properties. However, in select cases, we partner with leading institutional storage operators where we believe it is appropriate for specific assets and market conditions. Our affiliated operating platform is designed to reduce reliance on third-party property management where we are directly operating the assets.

Through SCM, we manage construction from ground-up development to value-add repositioning. This integrated structure is intended to create clearer accountability across key phases of the lifecycle while maintaining flexibility to engage external partners when it best serves the asset and investor outcomes.

Affiliated entities may receive fees as described in the offering documents. Investors should review all affiliate compensation and conflicts of interest in the applicable PPM.

Key Question to Ask

“Do you manage the property directly, or do you use a third-party property management company? If third-party, who is the PM, what are their fees, and what is your contingency plan if performance underperforms expectations?”

Underwriting Discipline: The Assumptions Behind the Numbers

A sponsor’s underwriting is only as good as the assumptions it rests on. Projected returns are outputs; the inputs (rent growth rates, occupancy trajectories, exit cap rates, and operating expense assumptions) are what actually determine whether those returns are achievable.

Rent growth assumptions

If the pro forma assumes 5% annual rent growth in a market that has historically delivered 2–3%, the projected returns are built on an aggressive foundation. Ask the sponsor to justify every growth assumption with local market data, comparable property performance, and third-party research.

Exit cap rate assumptions

The exit cap rate is often a significant driver of projected IRR, depending on leverage, hold period, and NOI assumptions. A 100 basis point difference in the exit cap rate can meaningfully swing projected IRR. Conservative sponsors underwrite exits at cap rates equal to or higher than the going-in cap rate, not lower.

Lease-up projections

For value-add or development deals, the timeline from acquisition or construction completion to stabilized occupancy is critical. Industry data suggests 36 months as a reasonable expectation for new self-storage facilities.[6] A pro forma that assumes 18-month lease-up in a competitive market is projecting an outcome that most operators would consider unrealistic.

Sensitivity analysis

A credible sponsor stress-tests their projections. They should demonstrate what happens to IRR, cash-on-cash, and equity multiple if occupancy underperforms by 5%, if rent growth is 1% lower than projected, or if the exit cap rate expands by 50–100 basis points.

Underwriting assumptions: red flags vs. green flags

What to look for when reviewing a syndication pro forma

Key Question to Ask

“What are the three most important assumptions in your underwriting, and what happens to investor returns if each one is wrong by 10–20%?”

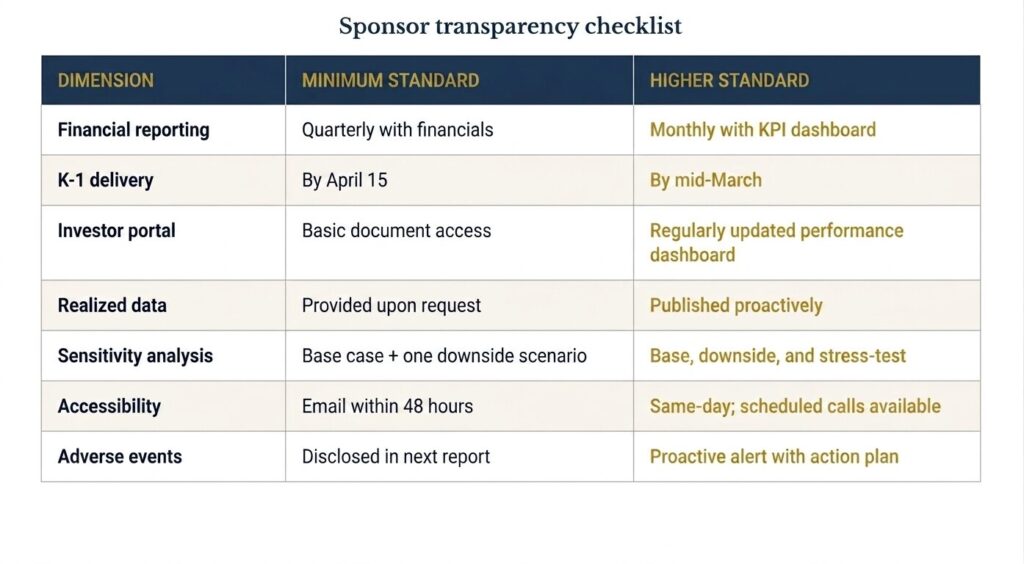

Communication and Transparency Standards

A sponsor’s communication practices before the investment are a reliable indicator of what you can expect after you commit capital. Transparency is not a marketing message; it is an operational discipline that manifests in specific, measurable behaviors.

Reporting cadence and depth

At minimum, expect quarterly reports that include financial statements, occupancy data, rent growth metrics, progress against the business plan, and any material changes to the investment thesis. Monthly reporting is a higher standard.

K-1 delivery timing

Schedule K-1s for real estate partnerships commonly arrive in March or later. Earlier and more consistent K-1 delivery may indicate stronger accounting processes, though timing can vary based on deal complexity and third-party tax workflows. Repeated unexplained delays may warrant follow-up questions about accounting processes and expected timelines.

Accessibility and responsiveness

Before investing, test this: send a detailed question about the deal structure or underwriting assumptions. The quality and speed of the response tells you more about the sponsor’s communication culture than their pitch deck ever will.

Bad news communication

Ask the sponsor: “Can you describe a time when a deal underperformed expectations? How did you communicate that to investors, and what actions did you take?” A sponsor who can speak candidly about challenges demonstrates the kind of transparency that protects investors.

Putting It All Together: The Due Diligence Framework

The five dimensions above are not a sequential checklist; they are a multi-dimensional evaluation that should be applied in parallel. The goal is not to find a perfect sponsor. The goal is to find one whose strengths, structure, and operational depth match the risk profile you are willing to accept, and whose communication practices give you confidence that you will know what is happening with your capital at every stage of the investment.

10 questions to consider before investing in a syndication

A structured due diligence conversation guide for passive investors

- Can you provide realized IRR, cash-on-cash, and equity multiple from all exited deals?

- How did your portfolio perform during the 2022–2023 interest rate environment?

- What percentage of equity are you personally co-investing in this deal?

- Walk me through the waterfall structure. When do you begin earning promote?

- Do you manage the property directly, or through a third-party management company?

- What exit cap rate are you assuming, and how does it compare to current market cap rates?

- What happens to projected returns if occupancy is 5% lower and the hold extends by two years?

- How often will I receive financial reports, and what metrics will they include?

- Can you describe a deal that underperformed and how you communicated that to investors?

- What is your debt strategy (fixed, floating, or hedged) and what is the interest rate risk?

The Spartan Standard

At Spartan Investment Group, we built our sponsor model around the five principles outlined in this guide, because we evaluated dozens of sponsors as investors ourselves before becoming one.

Track record

We believe realized performance history is one of the most credible indicators of underwriting discipline. We provide realized performance data from exited investments alongside projections for active deals.

Alignment

We risk our own capital alongside our limited partners. Where applicable, our promote may be structured above a preferred return hurdle, as described in the applicable offering documents, ensuring that our outsized compensation is earned only when investor outcomes exceed defined thresholds.

Operational depth

Through FreeUp Storage and SCM, we manage or oversee key dimensions of the asset lifecycle, from site selection and construction to revenue management and disposition. Our affiliated operating platform is designed to reduce reliance on third-party property management.

Underwriting discipline

We seek to underwrite with conservative assumptions, including stress-testing across multiple scenarios. We present base-case, downside scenario, and worst-case projections so investors can evaluate key sensitivities and risks based on their own circumstances.

Transparency

Our investors receive regular reporting with detailed financial and operational metrics. Our investor relations team is accessible, responsive, and forthcoming, especially when the news is not what anyone hoped for.

Ready to evaluate a real deal?

Review our current offering materials, past performance data, and sponsor credentials firsthand.

Disclaimer: This guide is for informational and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any security. Past performance is not a guarantee of future results. All real estate investments involve significant risk, including the potential loss of principal. Any specific offering is made solely through a Private Placement Memorandum (PPM) pursuant to Rule 506(c) and is restricted to verified accredited investors. Please consult with qualified legal, tax, and financial advisors before committing capital.

Sources:

- White Coat Investor. “How Do You Evaluate a Real Estate Syndication?”

- Accountable Equity. “What Is Real Estate Syndication? A Complete Guide for Accredited Investors (2026).” April 2026.

- Modern Storage Media. “2026 Self-Storage Outlook: 10 Industry Experts Speak Out.” March 2026.

- Accountable Equity. “Red Flags When Evaluating a Real Estate Syndication.” April 2026.

- Storeganise. “Investing in Self Storage: Complete Beginners Guide 2026.” March 2026.

- Wealth Formula. “Real Estate Syndication Due Diligence: What to Evaluate.” February 2026.