What Your K-1 Is Actually Telling You

Every spring, passive investors in real estate syndications receive a Schedule K-1. Most hand it directly to their CPA without a second glance. That is a missed opportunity. Your K-1 is one of the most information-dense documents you receive as an LP and understanding what it says can meaningfully change how you plan, invest, and file.

This guide walks through the lines that matter most, what they mean for your tax bill, and the patterns worth tracking year over year.

What a K-1 Is and Why You Get One

When you invest in a real estate syndication structured as a partnership or multi-member LLC, the entity itself does not pay federal income tax. Instead, it passes its income, losses, deductions, and credits directly to investors. The K-1 is how that allocation reaches you. It reports your pro-rata share of the partnership’s financial activity for the year and it feeds directly into your personal return.

Important: Do not file your personal return before all your K-1s arrive. Operators commonly deliver in March; complex fund structures can push that later. Filing early and amending costs more in accounting fees than the extension ever will.

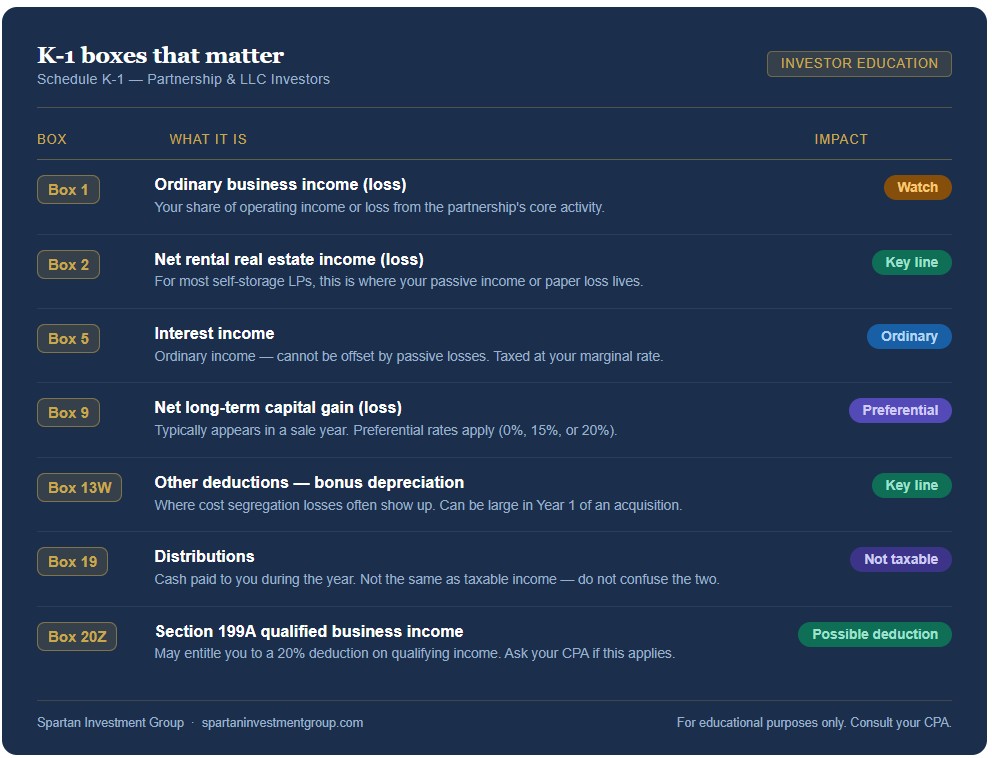

The Lines That Actually Matter

A K-1 has dozens of boxes. Most passive investors in self-storage deals will see activity in a handful of them. Here is what each one is telling you.

How Passive Income and Losses Flow

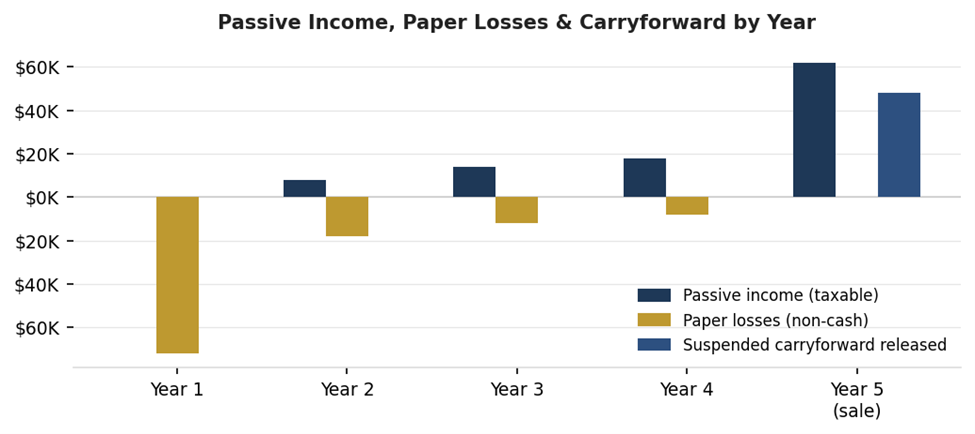

The most misunderstood aspect of K-1 investing is the passive activity loss rules. As a limited partner, all income and losses on your K-1 are classified as passive by default. That has two important consequences.

First, passive losses can only offset passive income, not your W-2 salary, not interest income, not dividends. If a cost segregation study generates a $50,000 paper loss in Year 1 but you have no other passive income, that loss does not disappear; it carries forward to future years and can offset passive distributions from that deal or others.

Second, when a deal is sold, any suspended passive losses from prior years are released and can offset the gain. This is one of the most valuable deferred benefits in syndication investing; but only if you have been tracking those carryforwards.

Illustrative example: a $500K LP position in a self-storage syndication over a 5-year hold. Year 1 cost segregation generates a large paper loss; passive income builds as operations stabilize; carryforward losses are released at sale in Year 5.

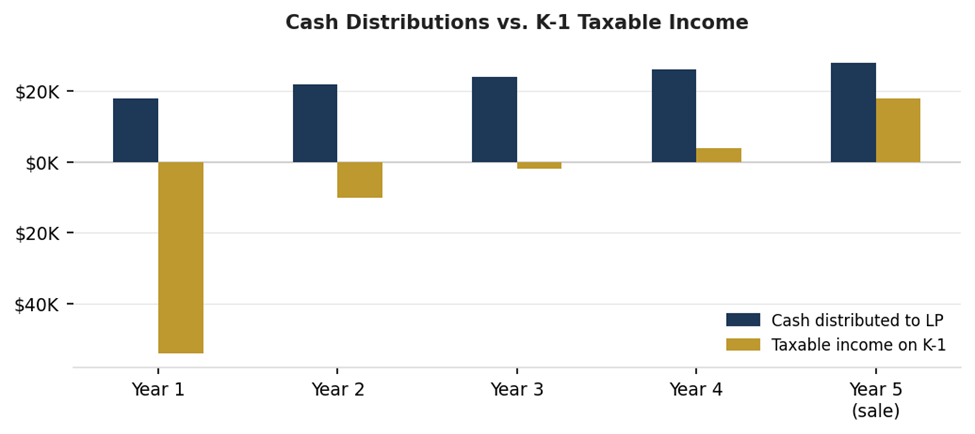

Distributions vs. Taxable Income. Not the Same Thing.

This is one of the most common points of confusion for first-time LP investors. You may receive $20,000 in cash distributions during the year and owe very little, or nothing, in tax on them. You may also receive a K-1 showing a $40,000 loss even in a year when the property performed well operationally.

That disconnect is driven by depreciation. When a cost segregation study front-loads large deductions in Year 1, the partnership’s taxable income can be deeply negative even if cash flow is positive. The chart below shows how this plays out for a typical self-storage deal.

Illustrative figures. Depreciation deductions create a gap between cash received and taxable income — particularly in Year 1 when bonus depreciation is largest.

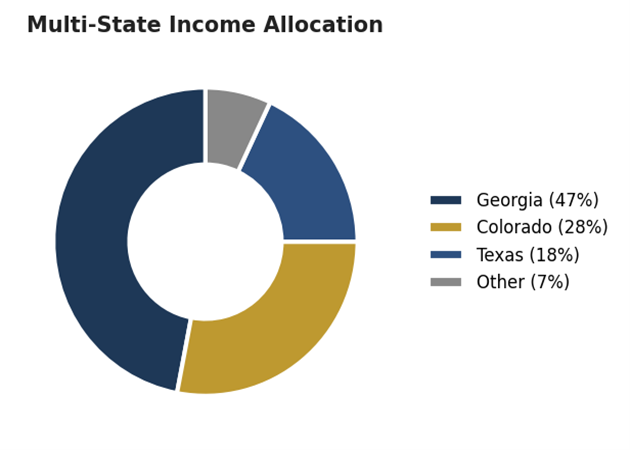

State Allocations: Do Not Skip This Section

If the fund owns properties in multiple states, your K-1 will include state-level income allocations. Modest allocations to states where you are not a resident can trigger nonresident filing obligations and ignoring state notices creates headaches that far outweigh the cost of filing a simple nonresident return.

Before handing your K-1 to your CPA, confirm: the states listed, the income allocated to each, and whether any of them are new compared to last year. A fund that acquired a new asset in a different state mid-year will add a state allocation you may not have seen before.

Example: multi-state income allocation from a single fund K-1.

* Every Spartan investor’s tax situation is unique. We strongly encourage working with a CPA experienced in real estate syndications to maximize your depreciation strategy.

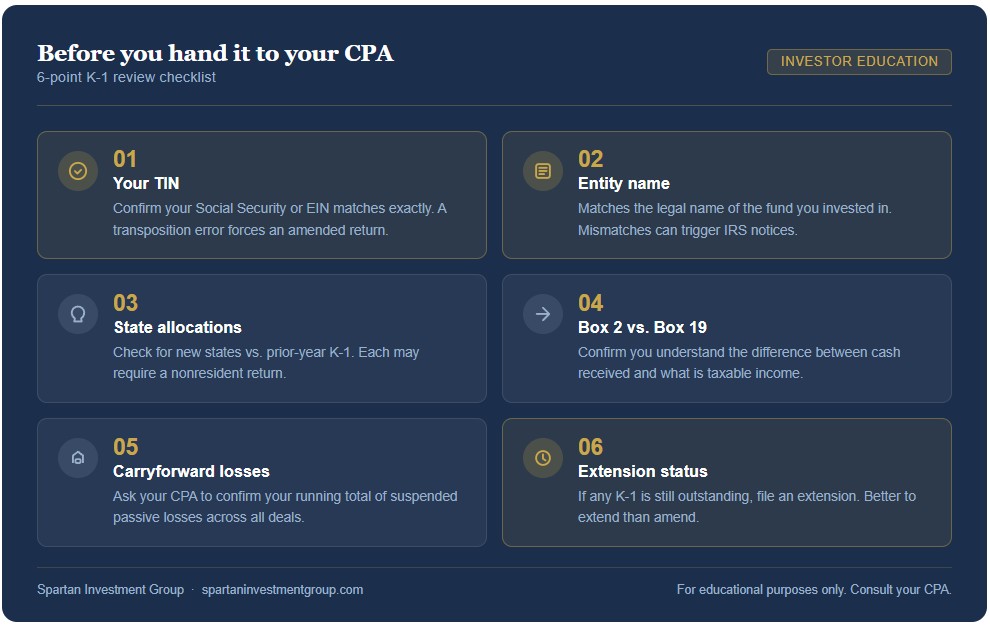

What to Check Before You Hand It to Your CPA

A three-minute review now can save hours of amended filings later. Before passing your K-1 along, verify:

The Bottom Line

Your K-1 is not just a tax document; it is a performance report. The numbers on it tell you whether your depreciation is flowing as projected, whether distributions are outpacing taxable income, and whether your passive loss carryforward is building toward a meaningful offset at sale. Investors who read it that way get more out of every deal and fewer surprises every April.

Ready to Deploy Capital with Spartan?

Join our investor community and access institutional-grade self-storage opportunities built for long-term wealth.

Disclaimer:

This material is provided for informational and educational purposes only and does not constitute tax, legal, accounting, or investment advice. The discussion reflects general principles of U.S. federal tax law as of the date of publication and may not apply to your individual circumstances. Tax laws are complex, subject to change, and dependent on each investor’s specific situation.

Any references to depreciation, cost segregation, bonus depreciation, passive loss rules, capital gains, depreciation recapture, or 1031 exchanges are illustrative only and are not guarantees of tax outcomes. Examples and hypothetical scenarios are for demonstration purposes and should not be relied upon as projections of actual results.

Investing in real estate involves risk, including loss of principal. Past performance does not guarantee future results. Investors should consult their own qualified tax and legal advisors before making any investment decisions.