Tax Season 2026: A Strategic Checklist for Self-Storage Syndication Investors

(For 2025 tax returns filed by April 15, 2026)

Missed tax benefits in real estate syndication rarely stem from a lack of available provisions. More often, the gap is procedural: rules with strict timing requirements, K-1s that arrive weeks into filing season, and assumptions about depreciation, passive losses, and state obligations that diverge from how partnership taxation actually operates. Tax Season 2026 presents a specific set of challenges for self-storage syndication investors filing their 2025 returns. Below is a practical, investor-oriented framework to review with your CPA before you file.

What to Review Before Filing Your Real Estate Syndication Taxes

1) Start with the Deadlines and the Reality of K-1 Timing

For individual filers, the federal deadline for 2025 returns is Wednesday, April 15, 2026. Real estate partnerships commonly deliver K-1s in March (or later). Filing too early can create amended returns and avoidable friction.

Practical move: Plan to file an extension to prioritize accuracy over speed. Shifting to an October filing deadline allows for late-arriving K-1s and prevents the “red flag” of an amended return, which statistically invites higher IRS scrutiny. By avoiding the April surge, you ensure complex depreciation and passive loss elections are documented correctly the first time, reducing audit risk while fulfilling your payment obligation by April 15.

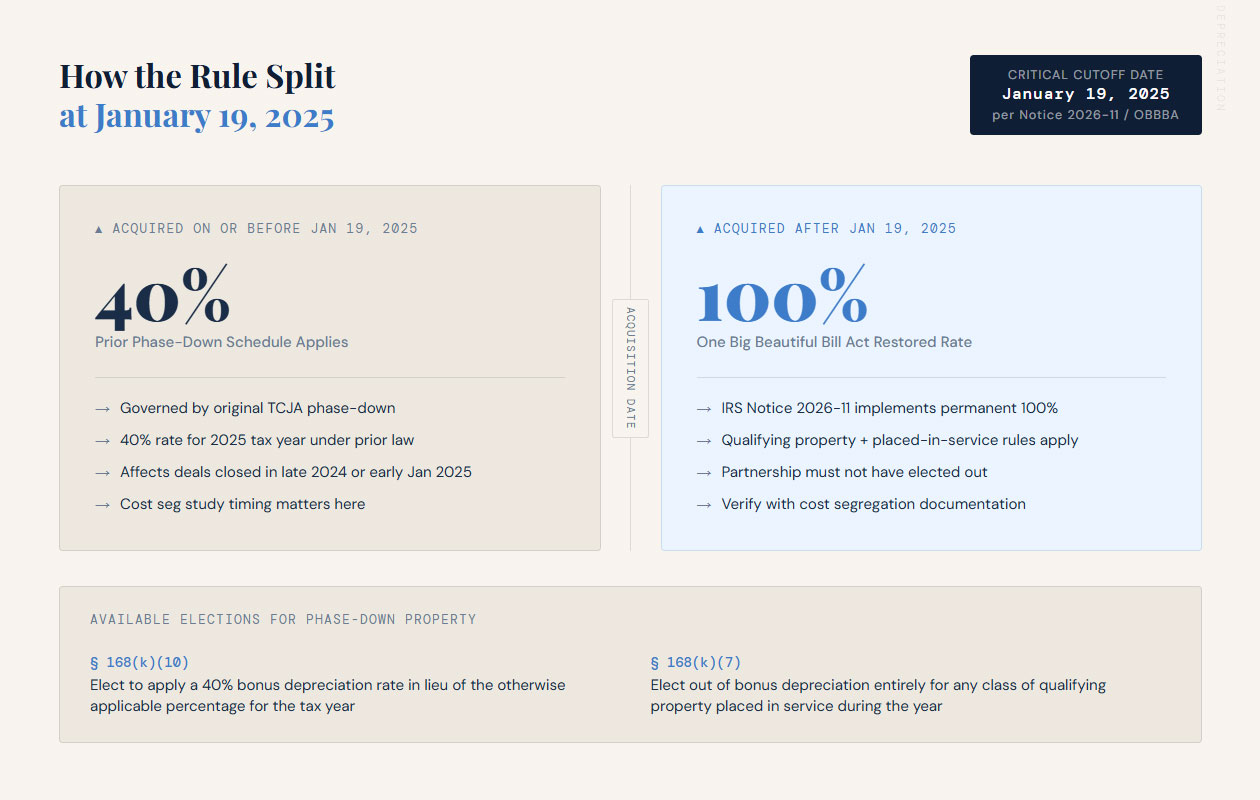

2) Bonus Depreciation: The Rules Have Changed – Confirm What Applies to Your Deal

The “Do This Now” Checklist (bring to your CPA)

Many investors still think in the “phase-down schedule” (80/60/40/20). That schedule was widely discussed, and still shows up in older planning content.

However, as of the 2026 filing season, the IRS has issued interim guidance (Notice 2026-11) implementing changes under the One Big Beautiful Bill Act (passed in 2025) that restore 100% bonus depreciation for certain qualifying property. The key rule: the 100% rate applies to property acquired after January 19, 2025 and placed in service under the updated election rules.

Property acquired on or before January 19, 2025 remains subject to the prior phase-down schedule: 40% for 2025. This distinction is critical for deals that closed in late 2024 or early January 2025.

What to verify (don’t assume):

- Did the partnership’s assets qualify under the updated rules, and when were they acquired/placed in service relative to the January 19, 2025 cutoff?

- Did the partnership elect out or elect a specific rate? (For property still subject to the phase-down schedule, elections may include 40% under Section 168(k)(10) or a full opt-out under Section 168(k)(7).)

- Was a cost segregation study performed, and if so, what year did it apply?

Operator note (self-storage-specific): Self-storage facilities often include significant shorter-life components (site improvements, electrical systems, paving, etc.). However, the tax outcome depends on what was purchased, when it was acquired and placed in service, and which elections were made. Treat this as a documentation-driven analysis, not a rule-of-thumb exercise.

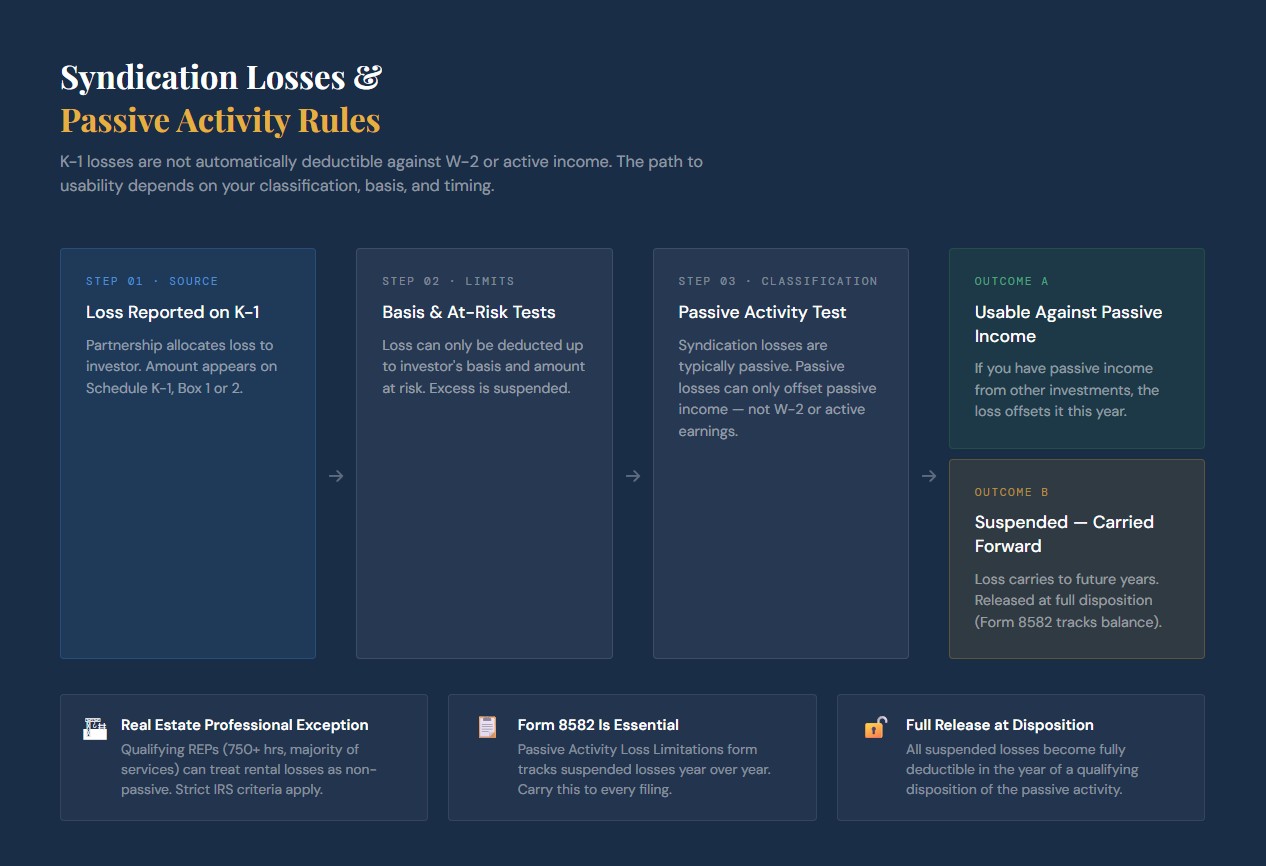

3) Passive Loss Rules: Depreciation Isn’t Always Usable This Year

A common mismatch: investors see large losses on a K-1 and expect them to reduce W-2 or active business income. In many cases, syndication losses are generally passive and can be limited; unused losses may carry forward under passive activity rules until they can be used (often against passive income or upon a qualifying disposition). The IRS summarizes these rules and points taxpayers to Publication 925 for the details.

What to ask your CPA:

- Were the losses deductible this year, or were they suspended and carried forward?

- Are there basis or at-risk limitations affecting deductibility (which are common in partnerships)?

- If you qualify as a real estate professional under specific IRS criteria, does that change the tax treatment?

Bottom line: For many high-income passive investors, the “win” is often tax deferral and loss carryforwards, not immediate W-2 offsets. (That’s not bad, just different than the headline.)

4) Multi-State Income: Small Numbers Can Create Real Filing Obligations

Self-storage portfolios can span multiple states. Your K-1 may reflect state-source allocations, composite filings, state tax withholding, or separate nonresident filing requirements depending on the structure and the state.

What to confirm:

- Did the partnership file composite returns or withhold state taxes on your behalf?

- Do you have nonresident filing needs in any state based on the K-1?

This is exactly where “it’s only a small amount” can still generate notices if ignored.

5) If You Invested via SDIRA or Another Retirement Account, Watch UBTI/UDFI

If your retirement account invests in a leveraged real estate partnership, you may have unrelated business taxable income exposure via debt-financed income rules (often discussed as UBTI/UDFI). The IRS explains the framework under IRC Section 514 and how debt-financed income is calculated.

What to check:

- Did the K-1 include Box 20, Code V (UBTI), or a supplemental UDFI schedule from the partnership? If so, your IRA may have a filing requirement under Form 990-T.

- Does your custodian handle the filings, or does your CPA coordinate them?

- Was the property leveraged at any point during the year (e.g., acquisition debt, refinances, or construction loans)?

Retirement account investments may involve additional compliance and planning steps investors should account for.

6) Depreciation Recapture: Plan Early, Not at Exit

Accelerated depreciation can improve after-tax cash flow in early years, but it may increase depreciation recapture or otherwise affect taxable gain at exit. Your CPA can model this based on your basis, depreciation taken, and expected exit scenarios.

Strategic use: Treat this as multi-year planning, not a one-year tax tactic.

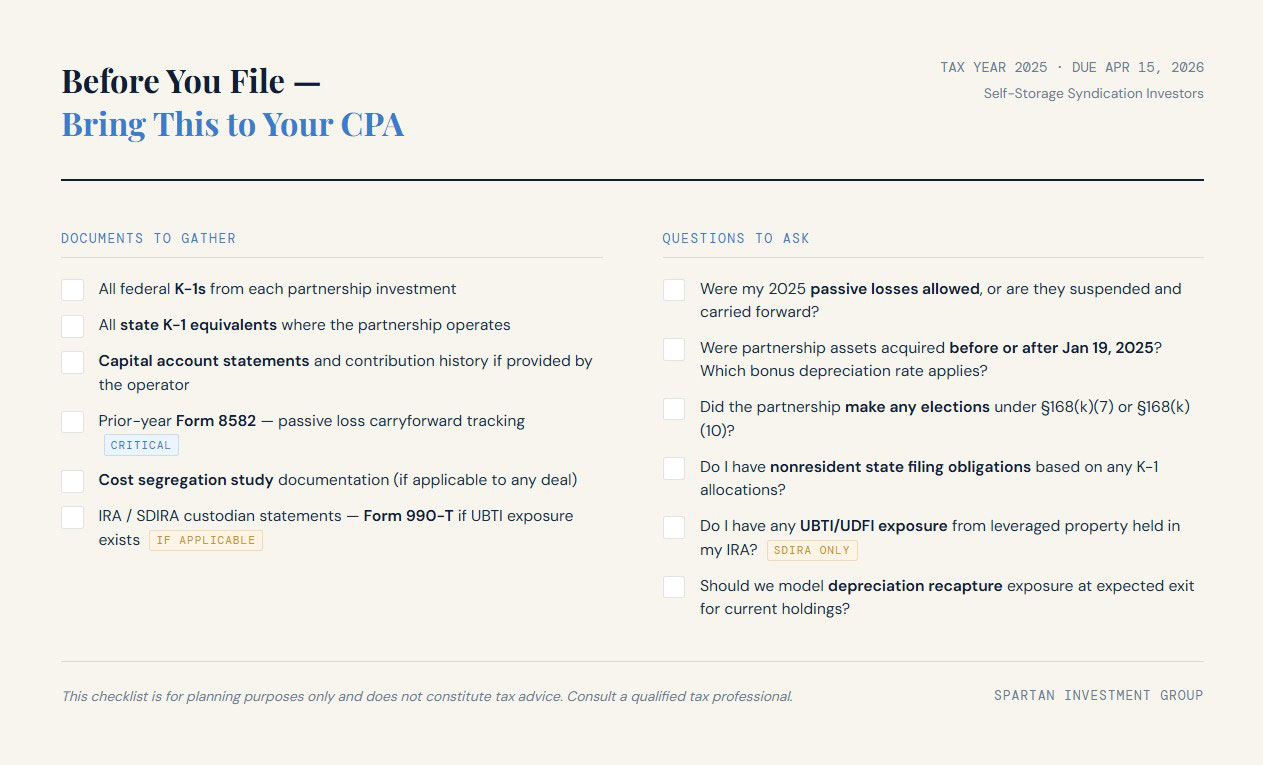

Documents to Bring to Your CPA (Real Estate Syndication Tax Review)

- All K-1s (and any state K-1 equivalents)

- Capital account statements / contribution history (if provided)

- Prior-year passive loss carryforward tracking (Form 8582, if applicable)

Key Tax Questions to Review Before Filing

- Were my 2025 losses deductible this year, or were they suspended under the passive activity loss rules?

- Did this partnership claim 100% bonus depreciation under the updated rules? When were the assets acquired relative to the January 19, 2025 cutoff? Did the partnership make any elections (e.g., elect the 40% rate or opt out entirely)?

- Do I have any state filing requirements related to this K-1?

- If the investment is held in an IRA, are there any UBTI/UDFI reporting requirements?

A Note on Tax-Benefit Expectations

If you’re a tax-incentivized investor, the highest-value posture is usually:

- Document-driven

- Timing-aware

- Conservative about what losses or deductions are usable today

- Clear-eyed about what carries forward

That approach avoids the two common problems: (1) overestimating current-year offsets, and (2) underutilizing legitimate carryforwards later.

Important Disclaimer:

This article is for educational purposes only and is not tax, legal, or accounting advice. It does not consider your individual circumstances, and it may not reflect state-specific rules or changes after publication. Spartan Investment Group does not provide tax advice, does not prepare tax returns, and does not guarantee any tax outcome. You should consult your own qualified tax professional regarding how these concepts apply to your situation and before making any tax-related decisions.

For a deeper look at self-storage investing, syndication structures, and tax considerations, visit our blog to learn more.