Market Analysis: What in Sam Hill is going on?

The stock market has been on a roller coaster ride for some time now, but the week of October 10th it nearly flew off the track.

Less than a year ago, in early November 2021, the Fed Funds Rate sat at less than 0.25%. This number feels as if it came from another planet as the Fed Funds Rate sits at 3.25% today.

What has led to this extremely volatile market environment? Many economists say that when the Fed makes a rate adjustment with the Fed Funds Rate or Prime Rate, it takes 12-18 months for the full effect to be felt by the economy.

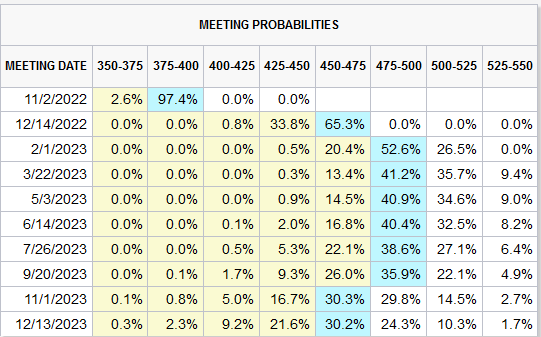

At the Jackson Hole symposium just over a year ago, Jay Powell, chair of the Federal Reserve, gave a lively speech espousing the secular disinflationary theme. At that point in time, the target rate for Fed Funds was 0 – 0.25%. Today, the forward target for the same metrics are shown below.

Fed Funds rate probabilities courtesy of CME group on 10-16-2022.

What’s unique about today’s market environment? Here are a few things that stand out to me:

- This is the first time this has ever happened. Never in history has the Fed raised the Fed Funds Rate in the face of an S & P 500 bear market—which occurs when a broad market index falls by 20% or more from its most recent high—such as it is doing presently.

- The Fed does not seem to be responding to a decrease in supply side inflationary pressures. History has forgotten that Paul Volker and his early 1980’s rate increases caused back to back recessions in 1980, 1981-1982 and a 3 year bear market in stocks which punctuated the 1968-1982 brutal sideways move in the equity markets.

Take Note: If you are near retirement, and the market goes flat for 14 years, and you withdraw 4% per year for 14 years, your portfolio is down roughly 45%. That’s with no loss due to market fluctuations. If the market drops by 20 or 30% while you’re making withdrawals – that’s a problem.

- The Fed does not seem to be responding to a decrease in supply side inflationary pressures. History has forgotten that Paul Volker and his early 1980’s rate increases caused back to back recessions in 1980, 1981-1982 and a 3 year bear market in stocks which punctuated the 1968-1982 brutal sideways move in the equity markets.

- Last Thursday, October 13th – the stock market had a wild day with the SPX swinging from an intra day low of 3,499 to an intra day high of 3,711. Trough to peak, this is a 6% move. This was due (WSJ Sam Goldfarb 10-13-22 6:47 pm) to a “recognition that recession risks are rising.”

- That’s nuts. That means that the news is so bad it’s good news for stocks. The end to the tightening cycle is then nearer?!

- That’s also why the I bond for November will likely have a lower coupon than the October issue. As the acceleration curve rolls over (decelerates) so does the new issue coupon.

Do you remember all the hubbub relative to the supply side of inflation? China’s ports locked up due to the strict “zero Covid” policy? Or how about this one, the Evergreen tanker that got sideways by way of its personal relationship with the Suez Canal in Egypt? Do we hear much about this type of news flow any longer? Not as much as we heard a year ago… Commodity prices by some analysts are in a bear market and freight rates have dropped precipitously.

Back to where we started with this short article, A) what’s unique about today’s environment and B) what may be important going forward.

- Never before has the Fed tightened monetary policy in the face of a technical bear market in the S&P 500 index. Never! Bear in mind (see what I did there) the stock market is a leading indicator.

- Inflationary pressures may be beginning to ease. If we fall into recession, strong cash flowing assets of a wide variety will likely gain value. Be sure you have a proper allocation to the asset class you believe to be in play.

As we all wrestle with current events, volatility, asset allocation and cash flow, be sure to keep perspective in mind. Sensationalism sells news, and the talking heads will talk as loudly as possible winding all that will listen as tight as possible. Having said that, Spartan’s base case on interest rates is articulated at minute 6:30 of this video. Seemingly, our base case is playing out as called.

A few decades ago, I had a framed quote by Warren Buffett on the wall of my office. It goes like this: “Turn off the economy, buy a business not a stock. Manage a portfolio of businesses.” I think that’s fitting in times like these. If we have a change of assumption by way of our base case on interest rates, we will let you know. As it stands today, our assumptions are unchanged.